By: Mamello Matikinca-Ngwenya, Siphamandla Mkhwanazi, Thanda Sithole, Koketso Mano

The International Monetary Fund (IMF) has published its latest set of macroeconomic forecasts, alongside a view on global financial stability and fiscal developments. Highlighted in all of these reports is the difficult era of elevated interest rates, debt, as well as physical and cyber risks. These all have a bearing on economic performance, which has already weakened on reduced total factor productivity. While activity in advanced economies will remain subdued by an anaemic demographic dividend, these economies are better protected from economic shocks. The resilience of emerging markets, however, stands to be tested. Here we summarise their latest views.

The IMF has once again raised its 2024 forecast and it now stands at 3.2%. At this rate, global growth will flatline between 2023 and 2025. Nevertheless, growth is expected to remain slow five years from now, at 3.1% - slower than the over 4% average between the year 2000 and the Global Financial Crisis (GFC) and 3.7% between 2010 and the Covid-19 pandemic shock. Within these headline growth dynamics, there is a gradual rise in advanced economy growth from 1.6% in 2023 to 1.8% in 2025, while emerging market growth slows slightly to 4.2% in 2025 from 4.3% in 2023. A better allocation of capital and labour to more productive sectors would support potential growth in future, coupled with productivity-enhancing capital investments such as Artificial Intelligence (AI). Commitment towards climate resilience and multilateral cooperation would also be helpful.

Further highlighting the relative resilience of advanced economies is the reach of inflation targets faster than emerging markets. Slower core inflation is pivotal for the disinflation trend and would reflect tighter monetary policy as well as softer passthrough of supply-side pressures and looser labour markets. Unfortunately, continued geopolitical tensions, with escalations in the Middle East, do not bode well for the inflation trajectory and could keep inflation elevated primarily through sticky goods and transport inflation. In such an event, delays in nominal rate cuts could become a feature of the forecast - compounding the "high-for-long" theme.

Despite heightened uncertainty, market volatility has been contained and expectations of a softer landing, slower inflation and lower nominal interest rates means that near-term financial stability risks have eased. Nevertheless, the difficult stretch of the disinflation process is still underway and adverse shocks could result in repricing of financial assets, reviving market stress and further exposing vulnerable sectors such as real estate. Furthermore, higher borrowing costs could exacerbate interest costs for overly indebted sovereigns and businesses - entrenching an environment of low growth by historical standards. Therefore, while there are signs that global financial conditions are loosening, caution needs to be applied by central banks where markets are too optimistic about the cutting cycle and could already foster easing ahead of monetary policy. In the longer term, economic fragmentations could reduce risk diversification, compounding other risks such as cybersecurity, and further weigh on financial and economic resilience.

In addition to this, restrictive monetary policy has not been coupled with tightened fiscal policy and the fiscal normalisation towards pre-pandemic levels has faltered. So, fiscal policy remains supportive of demand in overheated economies, leaving more of the work to slow inflation to monetary policy. While worsening fiscal metrices, higher interest rates must also cater for the flows required to cover deficits. Ultimately, the rebuilding of fiscal policy buffers would assist in insulating economies given weak growth in the medium term and the turbulence that can be expected from geopolitical tensions and climate change. In a nutshell, the global economy has been resilient, but adverse risks are material and should make rebalancing more difficult.

Week in review

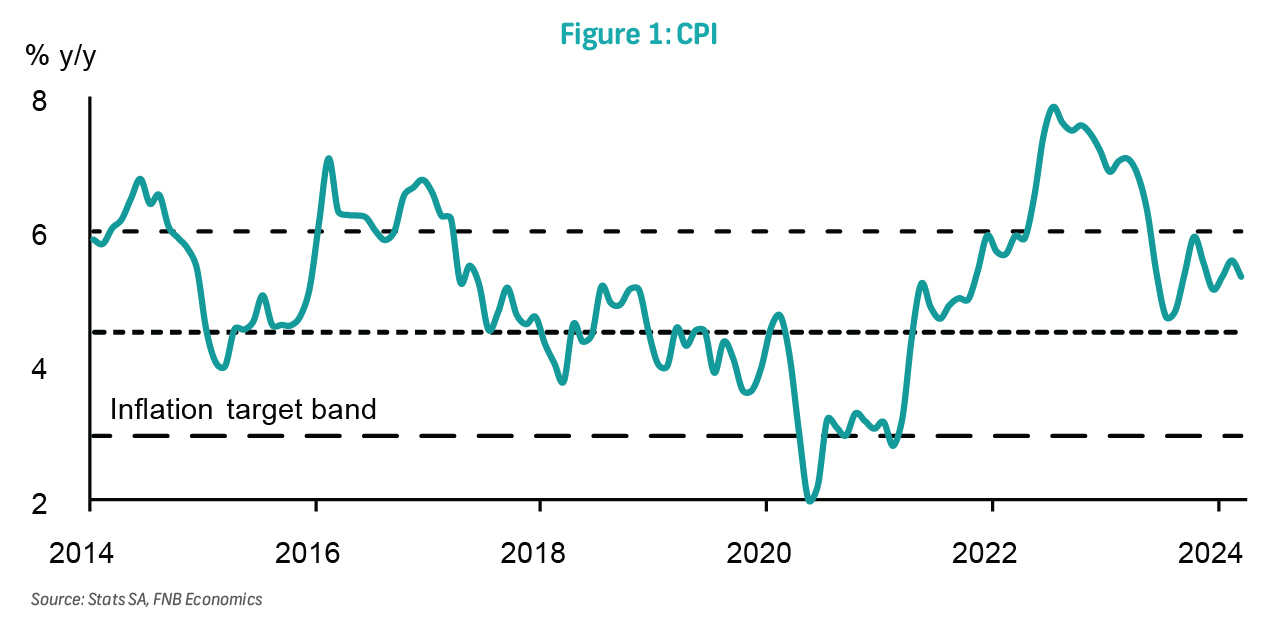

Consumer inflation slowed to 5.3% in March from 5.6% in February, with monthly pressure of 0.8%. Driving the monthly pressure was core inflation, which contributed 0.5ppts, while fuel added the other 0.3ppt. Core inflation lifted by 0.7% m/m and 4.9% y/y, primarily driven by education, housing, as well as alcoholic beverages and tobacco. Fuel increased by 5.3% m/m and 6.2% y/y, while food and NAB inflation continued to ease, settling at 5.1% y/y from 6.1% previously. We expect monthly pressure on headline inflation to slow in April as the weight of periodical surveys fall. Nevertheless, fuel inflation should continue to exert upward pressure to headline inflation. Annual headline inflation could remain flat at 5.3% y/y in April and average 5.2% over 2024. This view is threatened by hostile weather that has affected crop estimates, higher transport costs as geopolitical tensions remain elevated, as well as a weak rand if US interest rate cuts are delayed.

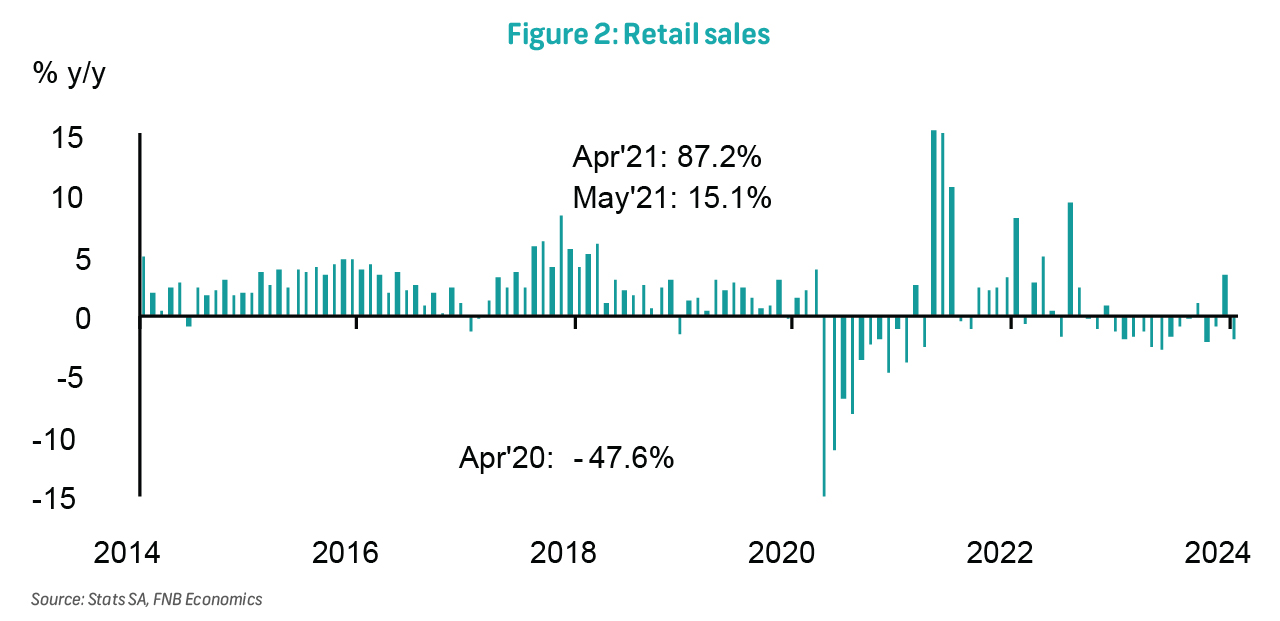

Retail sales fell by 0.8% y/y in February from a decline of 2.0% in January (revised from -2.1%). On a month-on-month basis, volumes rebounded by 0.4%, barely offsetting the 3.2% decline in January. Thus, volume sales in the last three months (Dec-Feb) are lower by 0.5% compared to the three months prior, implying that the retail industry is currently detracting from 1Q24 GDP growth. This means that the slight positivity in volumes growth signalled by the 1Q24 BER Retailer Survey is yet to reflect in official retail sales numbers. We expect the generally weak consumer demand environment to persist in the near term, driven by sticky inflation, high interest rates and depressed consumer confidence.

Week ahead

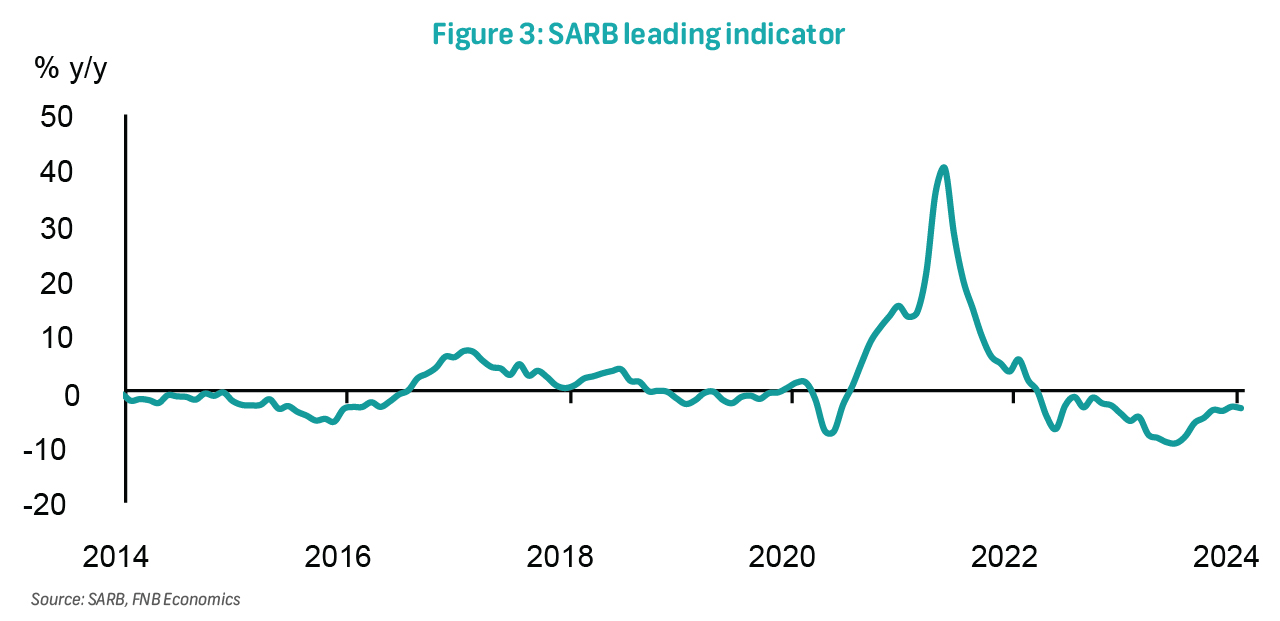

On Tuesday, the leading business cycle indicator for February will be released. The indicator fell by 0.5% m/m in January, marking the third consecutive monthly decline. This reflected a decline in seven constituent variables, which outweighed increases in the remaining three variables. Notably, the steepest declines were observed in the job advertisement space and average hours worked per factory worker. On a year-on-year basis, the leading indicator fell by 3.0%, marking twenty-two consecutive months of decline. While the level of the leading indicator is still above the pre-pandemic average, the protracted decline underscored enduring fragilities.

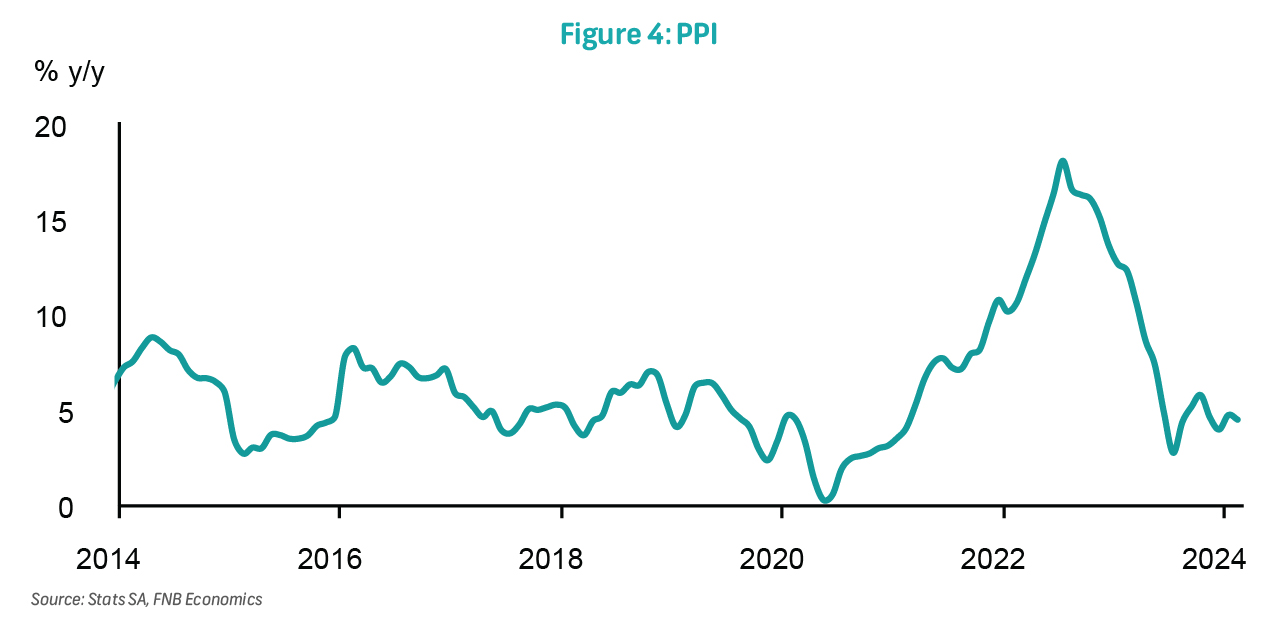

On Thursday, producer inflation data for March will be released. In February, production inflation measured 4.5% y/y reflecting a decline from 4.7% y/y in January. Monthly pressure escalated to 0.5% from 0.1% over the same period, fuelled by the 3.9% and 3.5% monthly increase in fuel and diesel prices, respectively. Excluding petroleum-related goods prices, producer inflation eased to 4.6% y/y (0.2% m/m) from 5.1% y/y (0.7% m/m). Intermediate producer price inflation, a measure reflecting product costs as they enter the production process, moderately rose to 1.0% y/y (0.8% m/m) from 0.2% y/y (0.7% m/m). Producer inflation is anticipated to have moderated to around 4.1% in March, with monthly pressure around 0.4%.

Tables

The key data in review

| Date | Country | Release/Event | Period | Act | Prior |

|---|---|---|---|---|---|

| 17 Apr | SA | CPI % m/m | Mar | 0.8 | 1.0 |

| SA | CPI % y/y | Mar | 5.3 | 5.6 | |

| SA | Retail sales % m/m | Feb | 0.4 | -3.2 | |

| SA | Retail sales % y/y | Feb | -0.8 | -2.0 |

Data to watch out for this week

| Date | Country | Release/Event | Period | Survey | Prior |

|---|---|---|---|---|---|

| 23 Apr | SA | Leading business cycle indicator | Feb | -- | 111.8 |

| 25 Apr | SA | PPI % m/m | Mar | -- | 0.5 |

| SA | PPI % y/y | Mar | -- | 4.5 |

Financial market indicators

| Indicator | Level | 1W | 1M | 1Y |

|---|---|---|---|---|

| All Share | 73,271.43 | -2.7% | 2.0% | -7.0% |

| USD/ZAR | 19.14 | 2.2% | 1.3% | 5.3% |

| EUR/ZAR | 20.37 | 1.4% | -0.8% | 2.4% |

| GBP/ZAR | 23.81 | 1.3% | -0.9% | 5.7% |

| Platinum US$/oz. | 934.87 | -4.6% | 4.5% | -14.2% |

| Gold US$/oz. | 2,378.25 | 0.2% | 10.2% | 19.3% |

| Brent US$/oz.. | 87.11 | -2.9% | -0.3% | 4.8% |

| SA 10 year bond yield | 11.57 | 0.1% | 2.3% | 7.2% |

FNB SA Economic Forecast

| Economic Indicator | 2021 | 2022 | 2023f | 2024f | 2025f | 2026f |

|---|---|---|---|---|---|---|

| Real GDP %y/y | 4.7 | 1.9 | 0.6 | 1.3 | 1.6 | 1.8 |

| Household consumption expenditure % y/y | 5.8 | 2.5 | 0.7 | 1.4 | 1.6 | 1.8 |

| Gross fixed capital formation % y/y | 0.6 | 4.8 | 4.2 | 4.4 | 4.4 | 3.8 |

| CPI (average) %y/y | 4.5 | 6.9 | 6.0 | 5.2 | 4.6 | 4.5 |

| CPI (year end) % y/y | 5.9 | 7.2 | 5.1 | 4.8 | 4.8 | 4.5 |

| Repo rate (year end) %p.a. | 3.75 | 7.00 | 8.25 | 7.50 | 7.00 | 7.00 |

| Prime (year end) %p.a. | 7.25 | 10.50 | 11.75 | 11.00 | 10.50 | 10.50 |

| USDZAR (average) | 14.80 | 16.40 | 18.50 | 18.70 | 17.70 | 18.30 |