Physical address

4 Merchant Place Corner Fredman Drive and Rivonia Road Sandton 2196

Postal address

PO Box 650149 Benmore 2010

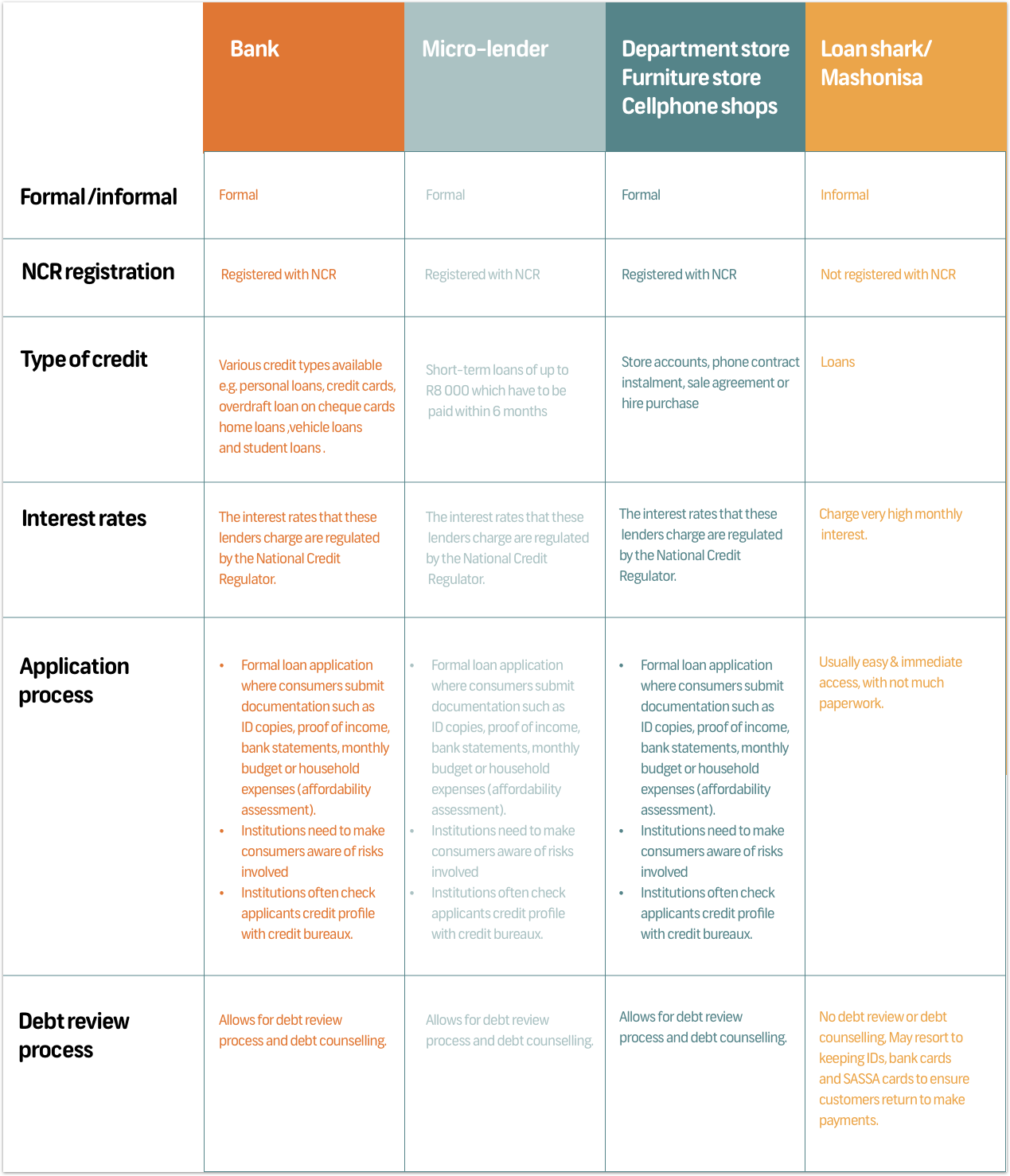

Where to

All these places offer different products and their terms and application requirements differ. The risk associated with each lender also differs, so think carefully before signing an agreement or contract.

There are two types of interest: interest earned (on savings and investments) and interest charged (on loans).

This type of interest is a way to grow your money and is a reward from the bank for saving your money with them. It's extra money you earn for saving your money with a bank or an investment/savings institution.

This is the type of interest charged by a credit provider to lend you money. It's the cost of credit and is usually calculated as a percentage of the amount that you borrow.

When interest is calculated on the original investment plus interest earned, so you earn interest on your interest, helping your money grow quicker.

When interest is calculated on the original amount borrowed invested plus any interest charged in previous months or years so you are charged interest on your interest, meaning your debt grows over time.

Taking up credit is a big decision. Before you do, consider the following:

Obtain a quote from the credit provider. It should show how much you will be paying in total.

Find out if there are penalties or rewards for repaying the debt earlier.

Get a copy of the contract and read it at home before you sign.

Make sure you understand the terms of the agreement.

Find out what will happen if you are unable to make the loan repayments on time.

The seller takes back the goods, as well as keeps the money you have already paid for the goods.

A judgement is a court order that forces you to repay your loans.

Depending on how big your debt is, the court can order that some of your property (such as furniture, a vehicle, etc.) can be repossessed.

The court will instruct your employer to pay a part of your wages or salary to the creditor as repayment of your debt.