Physical address

4 Merchant Place Corner Fredman Drive and Rivonia Road Sandton 2196

Postal address

PO Box 650149 Benmore 2010

After the all-in body attack that was January 2021, it's clear that the spread of Covid-19 and the associated global economic crisis will be competing for news headlines with eye-opening world events from vaccine nationalism to military coups, unprecedented presidential censures, disputed elections and feeding frenzies from retail investors.

Against this backdrop, we turn to our Chief Investment Officer, Patrice Rassou, to put some perspective on the year past and to highlight the big issues facing world markets in 2021.

Here at FNB, we stepped into 2021 with the outstanding news that we had been recognised as the Global SME Bank of the Year at the recent Global SME Finance Awards ceremony. The SME Finance Forum, which is managed by the International Finance Corporation, is renowned as a knowledge centre for data, research and best practice in promoting small-, micro- and medium-sized finance options. In addition, we have been named the Sunday Times' Best Business Bank in South Africa for the seventh consecutive year.

These achievements underline the innovation of our product and service offering and, as we head into this new year, it remains our aim to continue delivering top-class, world-beating solutions and convenient and secure digital channels.

Of course, relevant and quality advice remain the cornerstone of our offering, which is why we also include an analysis of the recent tax law changes in South Africa, specifically with regards to the country's policy around 'loop structures'. Many of these current changes are linked to government's focus on overhauling the current exchange control environment into a capital flow management system. Our focus is on what these changes mean for you?

Turning to opportunities on the horizon, an exciting inclusion for Africa-focused investors is an article exploring the growing interest in alternative assets and the opportunities inherent on the continent. Alternative investments across Africa are, traditionally, the domain of investment platforms such as venture capital, private equity or even angel investing, but we are also seeing pension funds edging into this space - particularly into investments such as renewable energy and infrastructure. It is also becoming clear that the roll out of digital infrastructure is another area of potential in an increasingly tech-focused future.

Until we meet again, stay safe.

Best wishes,

Eric Enslin,

CEO FNB Private Wealth

The human tragedy of 2020 was accompanied by an economic crisis as global economies shut down to try slow the spread of Covid-19. In addition, politicians in the developed world kept financial markets on edge over the year as an acrimonious United States election and the finalisation of the Brexit deal both went down to the wire. As we step into 2021, investors continue to be challenged in their long-term thinking as they contemplate whether a hazmat suit is still the only protection against a deadly virus. So, where to from here?

An eye on global markets

The global lockdown and halt to economic activity in the first half of 2020 floored all economies. Central banks unleashed unprecedented swift actions with a combination of aggressive monetary expansion and fiscal stimulus. Governments across the world tried their best to provide financial support to businesses and individuals, who saw their means of earning a living crushed unexpectedly. Interest rates around the world were pushed to the zero bound as central bankers aggressively cut rates and flooded capital markets with liquidity. The ploy was straight from the global financial crisis playbook - but on steroids - as the world's largest central banks did in a single quarter four-fold more quantitative easing than during the whole of the 2008 financial crisis. This approach will continue in 2021, with the new Biden administration in the United States planning more than US$2 trillion in stimulus with 80% of Americans likely to receive a stimulus cheque - an eye-popping number given that less than 20% do not work.

The bond market rally was followed by an equity market rebound. First, beneficiaries of the work-fromhome trend led the rally. But in the second half of 2020, as economies re-opened, a broader based rally ensued. With cheap money available, new participants joined the buying frenzy on several online apps - the so-called Robinhood effect. The amateurs jumped on the momentum bandwagon gobbling up Bitcoin and Tesla, racking astounding gains that are up more than 600% since March. These gains continued at the start of 2021 with Elon Musk briefly overtaking Amazon's Jeff Bezos as the wealthiest man on Earth.

The fourth quarter benefited from the additional fillip from the creation of vaccines, which added to the reopening trade. The S&P broke its record levels 33 times last year and the rally saw it rebound almost 70% from March lows.

The West Texas Intermediate oil price, which had turned negative earlier in the year, passed the more respectable US$50-per-barrel mark. Pharma stocks also attracted much interest, with Moderna up more than 200%. Globally, earnings declined by some 15% and valuation multiples expanded - but, as we know, markets wrote off 2020 and fixated on a more promising 2021.

Outing Agent Orange

In the United States, a blue sweep was regarded as a low probability outcome by most political commentators. While a Democratic win was seen as underpinning a much stronger fiscal response, this raised concerns about the impact of more aggressive fiscal action on the inflation. US 10-year yields spiked from record lows to end the year above 1% as inflation expectations also climbed. However, markets quickly shrugged off the impact of a contested election outcome even as outgoing President Donald Trump was making various erroneous claims about voting irregularities. Just as the Democrats were about to cement their control of the Senate after winning both seats in Georgia in January, Trump supporters stormed the Capitol - something unimaginable for a country born out of democratic principles.

After internet giants shut down Trump and his acolytes, who had instigated the riots, there have been many discussions about the role of social media in allowing 'alternative truths' to take hold in society. Trump's Make America Great Again campaign had become a proxy for a brand of nationalism and isolationism that was openly anti free-trade and anti-immigration. It also exploited the resentment caused by growing income inequality.

Local headwinds

South Africa's hard lockdown in April severely impacted the economy, which had been moribund for years. The R500 billion stimulus package (10% of GDP) failed to live up to expectations. The R200 billion loan support for small business was hardly drawn down and corruption took a bite out of some of the initiatives meant to combat the virus. Relative to the rest of the world, South Africa remains in a growth trap with constrained fiscal muscle but attractive real yields.

It should come as no surprise that South African bonds outperformed last year, posting very decent returns of 8.6%. The All Share made a strong comeback over the second half of 2020 to close the year up 7%. Despite being up some 21% in the finalquarter, property stocks lagged and were down 34% last year. Resources stocks remained the best performers for the year, up over 21% driven by strong commodity prices, with iron ore prices up an astonishing 77% as Chinese demand rebounded and supply remained constrained. Globally, the picture looks different with equities leading the way, up 22% in rand terms, while bonds were up 9% in rand terms (in large part due to the local currency's weakness).

The impact of the Covid-19 pandemic has also been exacerbated by the fact that lower income groups have been more vulnerable to the disease and suffered greater economic hardship in the form of job losses.

A role for green, sustainable investing

The coronavirus is just another example of a pathogen that has been transmitted from animals to humans. With human encroachment into natural habitats it is likely that we will see more outbreaks of this nature in the future. In addition, global warming has led to the migration of 70% of the world's animal species to cooler climates. The crisis has reinforced the fact that sustainable investing requires us to question the impact that companies have on the environment as well as society.

Internet companies have also come under the spotlight over their role in spreading fake news. Disinformation is now widespread, with some high-profile political campaigns - such as Brexit and Trump's election push - being underpinned by such disinformation. Right now, we are seeing the roll-out of Covid-19 vaccines being undermined by conspiracy theories.

Where to from here?

As the vaccine is rolled out in 2021, the human toll of the virus should stabilise and this should assist with the re-opening of economies around the globe. Then excess savings accumulated during the crisis will be put to work. Markets have already anticipated this, and valuations have discounted some of the good news. Global equities trade on a forward PE of 21 times compared with a long-term average of 18 times - which shows that the earnings rebound expected in 2021 has largely been discounted.

A world-class offering

In assessing the contenders, the international judging panel looked at the quality of the standard banking services available to FNB small business clients - such as top-class transactional, credit, invest and insurance capabilities - but also the additional valueadded services on offer.

The aim of the latter is to give self-employed customers and owners of SMEs easy-to-use resources that will help them to develop and grow their businesses, especially in the difficult and fast-evolving business environment of the pandemic. These resources are not merely financial in nature, but also assist FNB clients to recognise trends and capitalise on them by pivoting their offerings to cost-effectively meet new market demands.

"We don't see our role as merely providing a top-class banking platform. It's about taking a holistic view of nurturing and growing small businesses," explains Little.

Currently, small-, micro- and medium-sized enterprises (SMEs) make up 91% of formalised businesses in South Africa, according to the Banking Association. They employ about 60% of the labour force and account for more than a third of the nation's GDP

Small businesses are the cornerstone of South Africa's economic development and a potential salvation for job creation. So supporting this vital sector is an imperative for the country. FNB heard the cry and now our efforts have been recognised on the world stage.

The recent recognition given to FNB as the Global SME Bank of The Year for 2020 at the Global SME Finance Awards is an accolade not only for FNB and South Africa, but a benefit for the economy as a whole. The award has been made annually since 2012 and was won against stiff competition from top banks around the world.

This is the first time a financial institution from South Africa has won the award, says Gordon Little, CEO of FNB Commercial.

A world-class offering

In assessing the contenders, the international judging panel looked at the quality of the standard banking services available to FNB small business clients â such as top-class transactional, credit, invest and insurance capabilities â but also the additional valueadded services on offer

The aim of the latter is to give self-employed customers and owners of SMEs easy-to-use resources that will help them to develop and grow their businesses, especially in the difficult and fast-evolving business environment of the pandemic. These resources are not merely financial in nature, but also assist FNB clients to recognise trends and capitalise on them by pivoting their offerings to cost-effectively meet new market demands.

"We don't see our role as merely providing a top-class banking platform. It's about taking a holistic view of nurturing and growing small businesses," explains Little

Currently, small-, micro- and medium-sized enterprises (SMEs) make up 91% of formalised businesses in South Africa, according to the Banking Association. They employ about 60% of the labour force and account for more than a third of the nation's GDP.

The all-important National Development Plan envisages that this sector should create about 90% of all new jobs in the country by 2030. The current impact of Covid-19 on the economy â notably significant job losses in all sectors and particularly the increased shedding of positions by big corporates - makes the role of small businesses even more critical.

This, believes Jesse Weinberg, Head of the SME Customer Segment at FNB, makes FNB's offering all the more important at this critical juncture. "It's important to be more than just a bank. We want to go the extra mile and emphasise shared value with our clients. If they're successful, then we're successful," he says.

Extensive resources available to SME clients

Among the suite of resources available to selfemployed and SME clients are the following:

"When you bundle all of these offerings together and leverage them with the additional support that the bank provides, then you have a compelling offering for South African sole proprietors and SMEs, including those people who are looking to formalise their 'side hustle' into a viable business if they have become unemployed or under-employed due to Covid-19," says Little.

Helping SMEs to capitalise on emerging trends

"There is a totally different operating landscape for SMEs right now," observes Weinberg. "Almost without fail, they have to rethink route to market, how they market to clients, their relationships with staff, and their operational situations. They have to be lean and nimble in their decision-making."

Zinacare is one example of an SME client that has very successfully pivoted its core offering during the pandemic. A healthtechnology company that previously specialised in sexual health testing, it quickly added Covid-19 testing capacity and includes highly professional home testing in its offering.

For SMEs that are navigating the current �'new normal�', recognising and capitalising on emerging business trends is vital. Here the insights and mentoring resources provided by FNB play a valuable role.

In the SME market, says Weinberg, it's normal to talk about the 'three accesses': access to finance, access to market and access to education.

"Access to the customer has been completely turned on its head for many businesses," he explains. "If they can't trade via bricksand-mortar outlets anymore, what do they do? Go onto an online marketplace? Advertise online?"

Weinberg adds: "Many business people used to operate intuitively; now they find they are out of their comfort zone and their tradi tional areas of expertise. Perhaps they need access to finance and credit that they have never needed before? Maybe they should think about re-bonding their house?"

SMEs now need education and step-by-step advice more than ever, believes Weinstein. They require webinars, practical information and a new way of thinking in order to evolve their business model. This is where FNB's SME resources can help provide answers.

"There's a significant increase in the number of small businesses embracing e-commerce and digital enablement during Covid-19. So we see a lot of interest in our resources that deal with that aspect," he observes. "For example, we can guide them on how to start selling on Shopify and link up with Takealot for customer deliveries."

According to Little, one of the resources on Fundaba that can assist in this regard is a video interview with local Google experts, who discuss in simple and practical terms how to get your business noticed by customers on Google.

"There are a lot of those snippets on the platform. We work hard to ensure our content is fresh and userfriendly," he emphasises.

Among the other pandemic-related trends that could benefit SMEs is a clear preference by consumers to 'buy local' and support local businesses rather than large multinationals. There is also a move away from shopping in large regional malls â with their higherpriced premium global brands â to strip malls in local areas that offer good value.

Vumela Enterprise Fund assisting high-growth SMEs

Another way that the bank supports small business is through the Vumela Enterprise Fund. FNB Commercial, together with specialist SME investment company Edge Growth, manages the fund and through it makes equity investments into high-growth SMEs struggling to access finance through traditional channels.

Little says more than R300-million worth of equity and debt funding has been injected into small business through Vumela to encourage early-stage entities. "The idea is to focus on businesses that are making an impact in terms of job creation. We empower the shareholders to grow their businesses from a start-up into a more mature entity," he explains.

Interestingly, despite the perception of pandemicinduced business carnage throughout South Africa, there are surprising indications of resilience in the economy. Average turnover on FNB-held business accounts is, for example, back to where it was in February 2020 - before the pandemic struck.

Similarly, consumer spending patterns have rebounded strongly and, although they aren't quite back at prepandemic levels due to sectors such as tourism and hospitality being so heavily impacted, Little says you "get the sense that there is still some buoyancy in this economy".

This is, of course, good news for SMEs and for FNB's efforts to help grow the small business sector. "As a bank, we have put great effort into nurturing and advising SMEs. Not necessarily because it will be of immediate benefit to us, but because it is of long -term value to the country and our clients," stresses Weinberg.

Written by: Chantal Robertson, FNB Global Solutions Willem van der Merwe, Global Solutions Specialist FNB

South African Tax law stepped boldly into 2021; firmly in line with government's stated intention to modernise the country's existing exchange control system.

Last year the Minister of Finance, Tito Mboweni, announced Treasury's intention to transform the current exchange control environment into a capital flow management framework. This was first announced during the 2020 National Budget Speech, and essentially proposed an overhaul of exchange controls to take place over 12 months. To this end, three tax Acts were promulgated on 20 January 2021, of which certain sections address some of the exchange control changes:

The Tax Administration Laws Amendment Act holds particular interest fro from a wealth management perspective. Not least because it relaxes the country's policy regarding 'loop structures'.

What are loop structures?

A loop structure meant that South African residents were prohibited from holding any South African asset directly or indirectly through a non-resident entity. Inward loans were also prohibited.

A gradual relaxation to the loop structure restriction commenced in February 2018 when the South African Reserve Bank'�s (SARB's) reporting branch, Financial Surveillance (FinSurv) permitted a loop structure of up to a 40% investment by a corporate entity into a nonresident entity which would invest directly back into South Africa.

A further relaxation was announced on 30 October 2019 which permitted South African resident individuals to invest up to 40% in a non-resident entity that would invest directly back into South Africa.

In order to promote and encourage inward investment to South Africa, on 4 January 2021, the entire loop structure restriction was lifted, permitting South African individuals and South African entities to invest into an offshore structure which would invest back into South Africa.

Any loop structure created prior to these dates and in excess of the permissible percentage, must be regularised with FinSurv via an Authorised Dealer.

It is important to note that the South African Revenue Service (SARS) is simultaneously issuing legislation on the tax treatment of these structures. Therefore, from a cross-border planning perspective, it is key that both the exchange control and tax implications are considered carefully before making use of this latest SARB dispensation.

The finer details

While the abovementioned tax amendments were anticipated, it is notable that they apply from 1 January 2021. Therefore, effective immediately it is important to consider these amendments when making use of the loop relaxations or when making any change to an estate planning structure.

Rather than trying to punish those who implement the nowpermitted loop structures, the tax amendments are, in essence, aimed at closing possibilities to avoid tax.

To understand the changes, it is important to understand what is meant by a Controlled Foreign Company (CFC). In simple terms, a CFC is generally an offshore company of which more than 50% of shares are held by a South African resident. This resident can be an individual or a South African company.

Before the relaxation of the loop rules, a CFC would not have been allowed to invest in South Africa, as this would have been construed a 'loop structure', which was prohibited in terms of exchange controls. The tax amendments focus specifically on the rules dealing with the taxation of such CFCs, which will now be allowed to invest into South Africa.

When a CFC receives dividends from a South African company in which it owns shares, such CFC might benefit from a reduced dividend withholding tax rate, depending on the jurisdiction of the CFC and the terms of the double tax agreement between South Africa and the jurisdiction in question. Furthermore, when the CFC pays a dividend to the South African resident shareholder, such dividend could be exempt from tax. This would have created an obvious tax loophole when South African residents implement such a loop structure. The tax amendments provide that a CFC must now include a portion of a dividend received from a South African company in their net income (based on a formula). A reduction is received for dividend tax already paid. The amendment ensures that any dividends tax suffered upon the distribution of such a dividend by the South African company is considered. The South

African shareholder will also not be able to benefit from the di vidend exemption when receiving a dividend from the CFC.

Previously, when the South African shareholder sold the foreign share in the CFC to a non-resident third party, the capital gain was disregarded for taxation purposes. The amendments now provide that a South African resident shall not enjoy a capital gains tax exemption when selling shares in a CFC when the value of such shares is directly or indirectly attributable to assets in South Africa.

In line with treasury's long-term plan

The 2020 Budget Review outlined far-reaching changes to South Africa's exchange control system. Essentially, Treasury and the SARB are planning to replace the current system with a more user friendly and transparent capital flow management framework.

The main features of this new framework would look something like this:

These changes are squarely in line with global thinking. They also aim, with respect to changes on emigration, to align the treatment of South African residents and emigrants â thereby supporting the mobility of global citizens. Under the new proposals, natural persons (emigrants and South African private individuals) will be treated identically, subject to capital flow management measures.

The aim is to level the playing field between South African private individuals and emigrants, subject to tax obligations being met.

As Mboweni stated in his 2020 Budget Speech, it is also hoped that the changes will "open up new markets, promote regional integration [in light of South Africa signing the African Continental Free Trade Agreement] and contribute to economic growth".

What does this mean for you?

Broadly speaking, the new exchange control framework has implications for all South Africans, particularly those whom we refer to as 'global citizens' - those with interests abroad and investments offshore.

For our clients making use of the R1 million and up to R10 million offshore allowances, there will be little change to the current process. Individuals using the annual single discretionary allowance of R1 million for foreign investment purposes must provide a tax reference number. In addition, any use of the annual foreign investment allowance of R10 million requires tax clearance in terms of the SARS FIA001 process.

Any foreign investment transfers in excess of R10 million would require a special tax clearance process and would be subjected to a more stringent verification process, much like the current process. However, the latter process is also going to include assurance that the individual complies with anti-money laundering and counter-financing of terror requirements prescribed in the Financial Intelligence Centre Act, 2001.

What is important to consider is whether the tax changes outlined above would have an effect, and to what extent, on any proposed estate planning structure.

FNB's team of fiduciary specialist advisers can guide you through these discussions. For those looking to implement a structure benefiting from these relaxations, FNB has the ability via their offshore trust and fiduciary services provider, FNB International Trustees, to implement an offshore structure that can participate in the now-permitted structures. A fiduciary and structuring discussion should not be held in isolation and can benefit from the investm ent advice capabilities of FNB's wealth management team.

To initiate such a discussion please contact me, so that I can draw all the right experts from within our Financial Advisory and Global Solutions teams into the process.

As you grow and diversify your investment portfolio you will increasingly look beyond traditional assets such as stocks and bonds and towards the realm of alternatives; those private market assets that offer exposure to new approaches and markets. These opportunities are not as easy to access as picking a retail-focused investment off the shelf, which is why they are often the domain of venture capitalists and private equity experts, particularly in the African context.

"Even in South Africa you have the option of investing in private equity, but your options are quite limited," explains Chantal Marx, Head: Research and Content at FNB. "When it comes to investing in Africa ex-South Africa, you would more than likely have to be an ultrahigh- net-worth individual to tap into these options and you'd have to first identify which private equity or venture capital fund you want to 'back' to give you a decent return on of your investment."

Working with a private equity business with the likes of RMB Ventures, which invests in start-ups all over the African continent, is just one of doors open to investors looking to go this route. While RMB Ventures has a particular focus on funding both intellectual and human capital, other firms will offer a different approach and expertise across a range of sectors. This is why picking the right partner and investment avenue for your diversification ambitions is so important.

Different ways of investing

Alternative investments across Africa are, traditionally, the domain of investment platforms such as venture capital, private equity or even angel investing. In each instance, there are very clear reasons why these avenues are usually the preserve of the professional investor.

Marx explains: "Very few individual investors have the stomach for something like venture capital where, if you are really, really good you will only have a 20% success rate." This risk element is why, says Marx, the space has largely been the preserve of institutional investors and discretionary money.

That said, some pension funds are now edging into the world of alternative assets, particularly in investments such as renewable energy and infrastructure, which has a more certain return profile since the technology and processes you are investing in are tried and tested.

In the wake of Finance Minister Tito Mboweni's October 2020 Medium-Term Budget Policy Statement this trend may become even more of a factor - at least in South Africa â as the continued 'liberalisation' of Regulation 28 could see changes to exposure limits and guidelines for retirement saving investing into infrastructure projects. Currently pension funds can only invest 10% into alternative investments, including infrastructure, so these adjustments could create more opportunities for investors keen to explore alternative asset options.

In light of this drive, another option which is finding favour among some wealthy investors is a more hybrid approach that incorporates the tenets of venture philanthropy, which employs venture capital techniques and applies them to achieving socially focused goals. Marx explains: "For example, by investing in digital infrastructure in an area where there is no broadband access, an investor would likely make a pretty decent return due to the fundamental investment case, but they would also be investing in the upliftment of entire communities. For many, that broadens the appeal because the investment is actually making a tangible difference in the way that people live."

The opportunities

The roll out of digital infrastructure is just one area of potential. In the context of COVID-19, it is hardly surprising that healthcare is another important investment area.

Applying an alternative asset investment hat to this problem, explains Marx, means seeking to solve for a poor and underresourced African healthcare system not by following the old route of building brick-and-mortar hospitals by the thousands and trying to train doctors and nurses to see one person every 15 minutes, but rather by investing into telemedicine or digital medicine alternatives.

Similarly, she says: "If you think of learning, and the fact that a lot of kids don't have access to schooling, then perhaps your solution is investing in broadband infrastructure and digital education initiatives, rather than trying to build a school in every village."

The same goes for electricity. Instead of trying to build out electricity infrastructure that is focused around nuclear or gas or coal, investors could opt for direct investments into renewable energy, which is both cheaper and better for the environment.

Small-scale farming is another sector which is being galvanised across the continent thanks to innovations such as crowd farming platforms which connect smallholders to agricultural investors. This includes the likes of Nigeria's Farmcrowdy, which claims to have raised more than US$15 million for 25 000 farmers over four years, according to African Business magazine. Another agri-tech innovation highlighted by the magazine was South Africa's Livestock Wealth, which connects online investors with cattle farmers, or Ghanaian crowd farming firm Agripool, which negotiates leases on community-owned land to afford farmers legal protection.

The funding solutions being conjured through new online platforms are of particular interest, with Marx stressing that finding solutions in terms of funding for small-scale farmers is key to this African sector. "There is certainly a funding gap, since some larger institutions might not have the risk appetite to fund these smallscale farmers," she explains. "And yet there is a massive requirement for working capital every season. That means there is an opportunity - and a gap - there."

The challenges

While the opportunities are plentiful, there are very real challenges to this form of investment. Government buyin is one.

"When you are looking at something like agri-tech or broadband infrastructure or renewable energy, then the regulatory environment is supposed to aid those kinds of initiatives," explains Marx, "but in many cases they often hinder those kinds of initiatives."

Another issue, which is linked to the lack of liquid retail options, is that any investment is going to be tied in for quite some time.

Despite these concerns, Marx believes alternative asset investing certainly has a place in an emerging continent such as Africa. "What is great about going into areas that are relatively underdeveloped is you can use new techniques to solve for old problems in a much more efficient and cost effective way," she says.

FNB Connect has been offering exclusive SIM and smart device deals to FNB Private Wealth clients since 2015. Connect's improved quality network means that FNB Private Wealth clients can enjoy wider coverage on 3G and LTE networks and experience faster data connectivity than before. Clients can enjoy the following benefits of the FNB Connect SIM:

Garmin Fenix 6X sapphire

Lens Material: Sapphire Crystal Bezel Material: Diamond Like Carbon Coated Case material: Fiber-reinforced polymer with metal rear cover Strap material: 26mm quickfit silic

R689p.m.

x 24 months

Top Up Go

50 MB data,

15 voice minutes,

15 SMSs

Samsung Galaxy S21 256GB Dual Sim

The Samsung Galaxy S21+ 5G comes with a 6.7 inch touchscreen with 394PPI. It packs a 64-megapixel rear camera and a 10-megapixel selfie-camera. This is all powered by the Exynos 2100 International chipset and 8GB of RAM

R1439p.m.

x 24 months

Top Up L

2 GB data,

200 voice minutes,

300 SMSs

iPhone 12 Pro Max 128GB

Pro camera system with 12MP Ultra

Wide, Wide and Telephoto cameras, 4x

optical zoom range, Night mode, Deep

Fusion, Smart HDR 3, Apple ProRAW,

and 4K Dolby Vision HDR recording

R919p.m.

x 24 months

Top Up M

800 MB data,

100 voice minutes,

100 SMSs

Plus stand a chance to win 1 million eBucks when you buy any Apple product between 1 - 31 March 2021 at the eBucks Shop or FNB Connect

Ways to enter:

*Competition ends 31 March 2021.

Valid while stocks last. Product and Deal T& C's apply

During the past quarter South Africans have been bombarded with news of economic malaise, lockdown blues and news headlines highlighting the plight of many people as a result of the containment measures put in place to fight the current pandemic. It's hard to stay positive and see the light at the end of the tunnel, but there are green shoots which we can, and must, celebrate.

The first is the unwavering generosity of South Africans, which FNB Private Wealth and the greater FirstRand Group have witnessed in the flood of donations being made to our South African Pandemic

Intervention and Relief Effort (SPIRE) initiative. We thank each and every one of you who has made a contribution for your humanity, your care and your kindness.

In this newsletter we highlight another focus on caring for elderly communities and specifically those in old age homes by providing much-needed personal protective equipment. We provide details of how you can donate to this worthy cause, either by making a cash donation or by contributing your eBucks.

For our clients who are retirees or who are knocking on the door of retirement, we are also delighted to share some good news: in the form of our new Retirement Solution offering. Given the pressure on retirees, many of whom are seeing their monthly incomes eroded as a result of market movements and interest rate cuts, we have created an option which not only offers support during the immediate COVID-19 crisis but also offers long-term benefits in the form of preferential rates, private banking perks and tangible rewards.

FNB Private Wealth is not the only organisation adapting to the pressures of the moment. With uncertainty around incomes and with livelihoods under pressure, many South Africans are turning to the 'side hustle' to augment their incomes. Keen to know more, we enlisted the help of Nic Haralambous to talk us through this concept and to share his insights on this dynamic aspect of our future economy.

Of course, when it comes to navigating this strange new world, there are considerable stressors at play. Therefore, we are happy to outline some of the insights that author and human potential expert Nikki Bush shared with our staff and clients during a well-attended webinar. She offered both insights and recognition of the feelings of frustration and angst, which are welling up in us all. By applying her tips, it is possible to find that illusive balance.

We also hope you will find value in the insights from global strategist and speaker Abdullah Verachia, whose new book, Disruption Amplified: Reset. Rewire. Reimagine Everything, outlines the shifts impacting the profound changes playing out globally and who gives us a taste of how virtual engagements will evolve in the months and years to come.

The world, says Verachia, is not in the midst of a 'new normal' but a new. And this brings countless opportunities. One is in the agriculture space where the impact on global supply chains is creating potential for Africa's agricultural sector.

Stay well, stay safe and stay strong.

CEO, FNB Private Wealth

eBucks Lifestyle has teamed up with Wade Bales Fine Wine and Spirits, to bring you three exclusive wine offers for discerning FNB Private Wealth clients.

PAY WITH YOUR FNB CARD, EBUCKS OR A COMBINATION OF BOTH.

1. South Africa's First Growths

6 bottle case @ R1650

Receive 1 bottle of each of these

6 wines @ R998 (Save 40%)

Klein Constantia Cabernet

Sauvignon Shiraz 2016

Delaire Graff "De Caelo" Red

Blend 2016

Rust end Vrede Estate Syrah 2014

Rustenberg Peter Barlow 2015

Tokara Reserve Cabernet

Sauvignon 2014

De Toren Z 2014

(High profile producers with long track records of premium quality.)

2. Prestige Red Collection

6 bottle case @ R650

Receive 1 bottle of each of these

6 wines @ R398 (Save 40%)

Buitenverwachting Meifort 2012

Waterkloof Circle of Life Red

2011

Bilton Sir Percy 2009

Mischa Estate Shiraz 2014

Le Riche Private Blend 2015

Louis Strydom Shiraz Cabernet

2016 (Ernie Els)

(Rare and Exclusive reds selected for their remarkable value for money.)

3. Premium Imported Bordeaux

6 bottle case @ R2 300

Receive 2 bottles of each of these

3 wines @ R1 380 (Save 40%)

Chateau Potensac 2011

Prelude de Frombrauge 2014

Les Allees de Cantemerle 2014

(Just landed from France, these are classic Bordeaux blends of predominantly Cabernet Sauvignon and Merlot.)

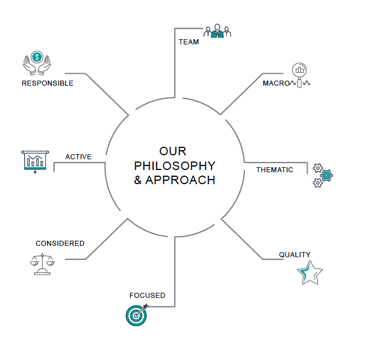

Few would argue that the foundation of successful investing hinges on a deep understanding of the global macroeconomic environment. But that's not all. It also necessitates a quality approach, one which considers investing in robust assets - companies of substance that can hold firm during economic cycles and which are best equipped to generate long-term sustainable revenues. And it requires a focused approach built around the concept of diversification.

That's the investment philosophy which has long underpinned the approach shared by FirstRand experts across the FNB, Ashburton and RMB brands. But now, under new Wealth & Investments and Ashburton Investments CEO Sizwe Nxedlana, this asset management position is being streamlined, better coordinated and geared towards client-centricity and ease of use. It's the same core philosophy in action, but with a maturation of processes, platforms and tools.

Our approach to asset management

In a nutshell, explains Nxedlana: "Our approach is about quality, at a reasonable value. It is macro-cognisant and we are long-term investors."

In the past, FirstRand's asset management communication approach focused heavily on the macro-economic aspects of sound investing, but this has never been the full and complete story of what goes on behind the scenes. "Now we have become a little more explicit about what we do and we are elaborating on our entire investment process and what this has to deliver to our clients," explains Nxedlana.

In practice, this means a greater emphasis on the environmental, social and governance (ESG) factors which are used to measure sustainability and the social impact of an investment. "We are about quality and when we invest your money we want to make sure we are investing in quality companies that are socially conscious, are governed appropriately and which take cognizance of environmental factors; because we think those are businesses that will be sustainable," says Nxedlana.

A great deal of attention is paid to quality screening across this investment process, to determine a viable universe of both onshore and offshore investment options. The next step is to undertake a detailed valuation effort to get into the nitty-gritty of the company in question to determine its quality and if it is valued appropriately.

Says Nxedlana: "We are doing a lot of work to make sure our valuation models are in place and are modernised." Drawing on the group's macro-economic expertise is certainly a critical consideration within these valuation models, allowing for long-term investments which, when made, can form part of a portfolio for as long as possible in order to reap the utmost benefit. With all these elements in place, there should ideally be no need for chopping nd changing of portfolios.

So what's new?

While this philosophy has long underpinned the FirstRand investment process, advanced plans are afoot within the broader group to bring all the strands of investment expertise together to streamline processes and create a highly client-centric experience.

Nxedlana took on the role of Ashburton Investments CEO in October 2019, alongside his existing role of CEO of Wealth and Investments. This move exemplifies the group-wide approach to leveraging it's platform capabilities in order to deliver the right investment solutions and to better meet client needs.

Explaining the dual role in more depth, alongside his focus on integrating FirstRand's investment capabilities through a single investment process and unified digital platform, Nxedlana explains that the current approach is being directed at getting the most out of the strong capabilities within the group and finding more efficient and effective ways to execute investment management more tightly.

"We have capability, which sits in a variety of places, and we are now really focused on understanding what the client's investment problem or investment need is across all the segments we have; that's across retail, commercial, corporate and institutional. Within that I also include intermediaries like independent financial advisors and direct fund managers," he says. The aim is to build on an existing culture of solving for client needs but doing so in a more deliberate and more co-ordinated manner.

What sparked this shift?

From the days when Laurie Dippenaar, GT Ferreira and Pat Gross founded a small financial structuring house in Johannesburg back in 1977, the FirstRand legacy has evolved into one of innovation and entrepreneurship. This has been evident in the growth and development of the various business units operating under the FirstRand banner. But organisations mature and, when they do, their systems and processes must do the same.

Nxedlana explains: "Now the organisation is being tilted on the side to emphasise client first, after all we potentially have clients who bank with us, lend, invest and take out insurance. The starting point for this new way the group is operating gives us the chance to pull together more. In the past we certainly collaborated, but we are now enhancing the coordination between the various business units that have grown up and been built within the group."

While some capabilities were born in different areas of the group for specific reasons, the idea now is to create an easier, more efficient and more effective offering for clients.

"As we have matured in terms of our focus on investment in the retail world, we've actually found that there is a lot of capability that sits within FirstRand in the likes of Ashburton and RMB and which, if we coordinated this better, would ensure a more efficient way to package solutions and also to distribute more efficiently, seamlessly and cost-effectively to clients," says Nxedlana. "Ultimately, we are building the business through understanding client needs, across segments and not just within certain business units.

Putting it simply: "We are trying to solve investment needs."

The COVID-19 pandemic has reshaped everyday business and lifestyle norms on a global scale. While Africa is remarkably resilient, we will need to work together to find creative solutions for our path to recovery.

For FNB, having a strong organisational purpose has never been as important. Our undertaking to liberate diverse talent to do good business for a better world provides a guiding light. We know that some of the best solutions come from multi-disciplinary teams, ensuring that innovation flourishes in the context of traditional values and social responsibility.

We are deeply invested in South Africa and the growth of its economy. Our dedicated banking and sector experts are partnering our clients, especially those businesses, sectors and communities most affected by COVID-19, to navigate this difficult landscape.

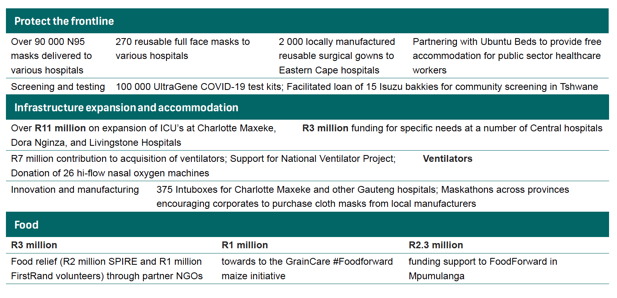

By combining the power of our people, capabilities and networks we are helping to create and sustain financial and societal value for our employees, stakeholders and clients. FirstRand has established a relief effort called SPIRE (the South African Pandemic Intervention and Relief Effort). As a driver and partner of FirstRand's relief effort, we are working with government, the business community, philanthropists and society to scale up critical medical infrastructure and prepare the country to manage the health and economic impacts of COVID-19. FirstRand has so far allocated an anchor investment of R100 million to SPIRE, funded by the FirstRand Foundations, FNB and RMB. Some of the key SPIRE projects below.

Should you want to get involved or contribute to the SPIRE fund, please include a reference with your transfer which indicates your province using two letters and, if relevant, a

specific initiative using the above codes and your name or business name.

For example: KN/CARE/ABC Ltd.

SPIRE fund banking details:

FNB account name: SPIRE

Account number: 62847932705

Reference: As per above example -

province/code/name or business name

(KN/CARE/ABC Ltd)

Should you want more detail on a specific initiative, please reach out to us and we can set up a session with the team dedicated to the particular project.

SPIRE is working closely with, and in support of, the Solidarity Response Fund.

While these partnerships represents a way of stretching rands during a difficult financial time, for those individuals lucky enough not to need this boost it is also possible to donate your eBucks if you would like to help nurses and front line through the Ubuntu Beds partnership. eBucks can be donated via the FNB App under 'Donate Now' or online through the eBucks website via the eBucks Shop.

We appreciate your contribution. We value your care. We salute your citizenship.

During the past quarter South Africans have been bombarded with news of economic malaise, lockdown blues and news headlines highlighting the plight of many people as a result of the containment measures put in place to fight the current pandemic. It's hard to stay positive and see the light at the end of the tunnel, but there are green shoots which we can, and must, celebrate.

The first is the unwavering generosity of South Africans, which FNB Private Wealth and the greater FirstRand Group have witnessed in the flood of donations being made to our South African Pandemic

Intervention and Relief Effort (SPIRE) initiative. We thank each and every one of you who has made a contribution for your humanity, your care and your kindness.

In this newsletter we highlight another focus on caring for elderly communities and specifically those in old age homes by providing much-needed personal protective equipment. We provide details of how you can donate to this worthy cause, either by making a cash donation or by contributing your eBucks.

For our clients who are retirees or who are knocking on the door of retirement, we are also delighted to share some good news: in the form of our new Retirement Solution offering. Given the pressure on retirees, many of whom are seeing their monthly incomes eroded as a result of market movements and interest rate cuts, we have created an option which not only offers support during the immediate COVID-19 crisis but also offers long-term benefits in the form of preferential rates, private banking perks and tangible rewards.

FNB Private Wealth is not the only organisation adapting to the pressures of the moment. With uncertainty around incomes and with livelihoods under pressure, many South Africans are turning to the 'side hustle' to augment their incomes. Keen to know more, we enlisted the help of Nic Haralambous to talk us through this concept and to share his insights on this dynamic aspect of our future economy.

Of course, when it comes to navigating this strange new world, there are considerable stressors at play. Therefore, we are happy to outline some of the insights that author and human potential expert Nikki Bush shared with our staff and clients during a well-attended webinar. She offered both insights and recognition of the feelings of frustration and angst, which are welling up in us all. By applying her tips, it is possible to find that illusive balance.

We also hope you will find value in the insights from global strategist and speaker Abdullah Verachia, whose new book, Disruption Amplified: Reset. Rewire. Reimagine Everything, outlines the shifts impacting the profound changes playing out globally and who gives us a taste of how virtual engagements will evolve in the months and years to come.

The world, says Verachia, is not in the midst of a 'new normal' but a new. And this brings countless opportunities. One is in the agriculture space where the impact on global supply chains is creating potential for Africa's agricultural sector.

Stay well, stay safe and stay strong.

CEO, FNB Private Wealth